Simple modular homes built with future additions in mind can change how builders think about scope, and timing and home value.

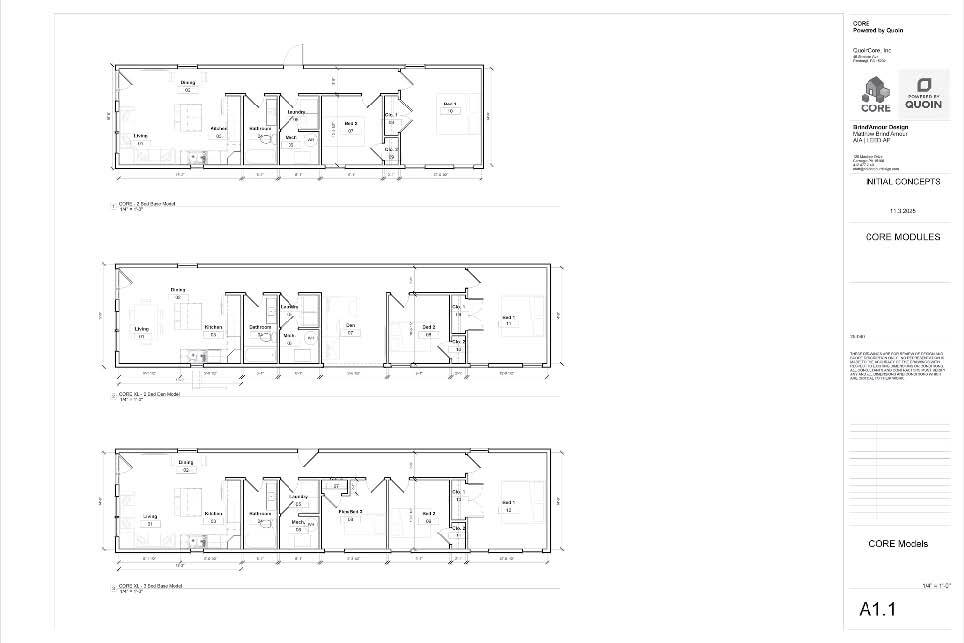

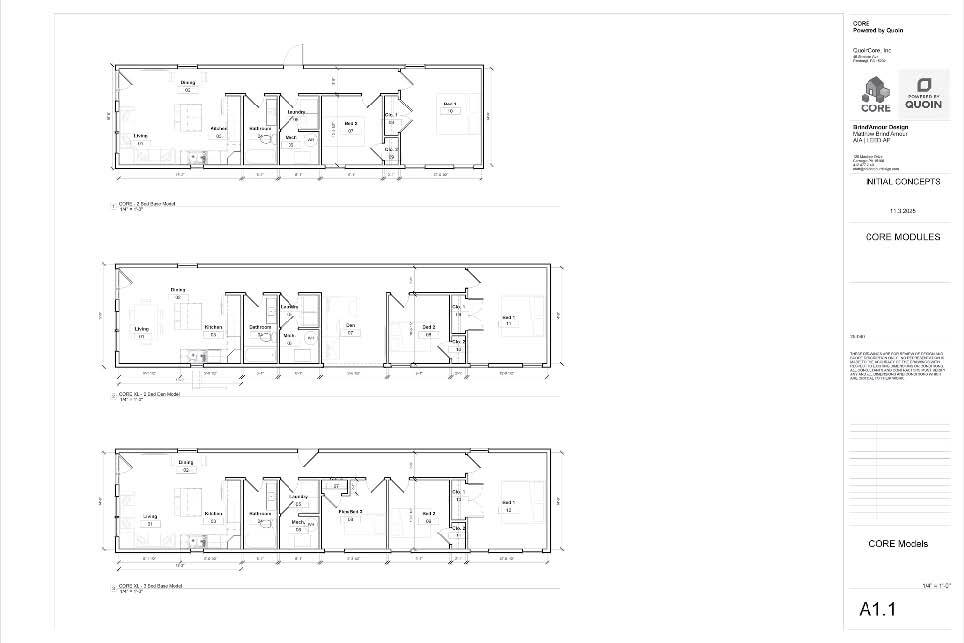

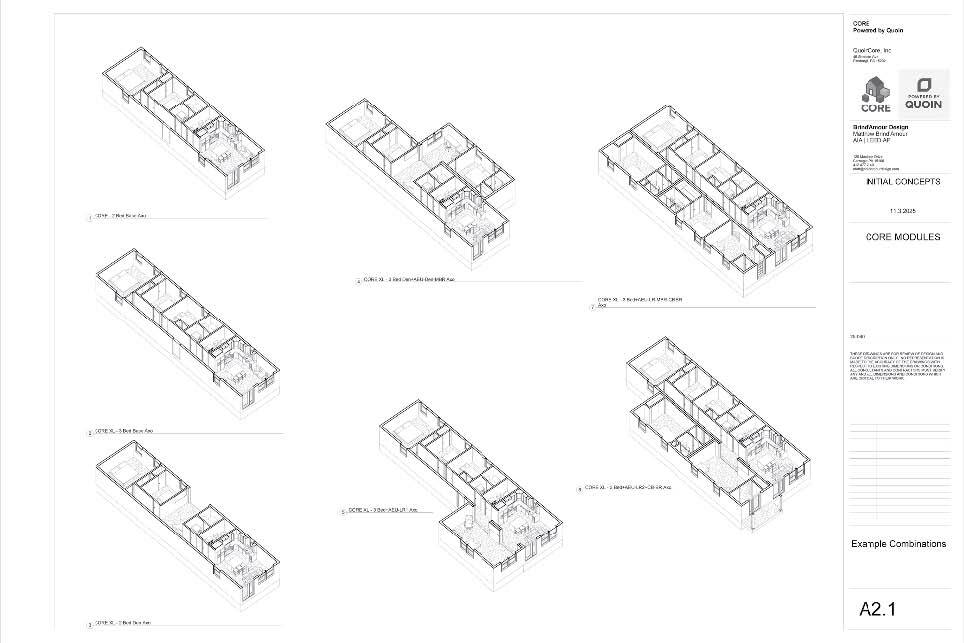

• Blockhouse’s CORE platform includes a fixed modular base unit and add-on modules. It supports factory repeatability and controlled customization.

• Pre-framed “portals” and preplanned MEP connections let homeowners add rooms as their budget permits, with minimal demolition and disruption.

• The platform allows builders to offer homes for a lower entry price while maintaining the promise of future margins.

Andrew Holmes, Chief Design Officer at Blockhouse Residential in Pittsburgh, Pennsylvania, is clear about the housing challenge. The way he sees it, it’s not so much an affordability problem as it is a profitability one. His solution is to take a longer-term view of profit.

“Homes cost what they cost to build,” he says. Materials, labor, insurance, overhead, compliance and risk must all be covered, and in the end, builders must make a profit. “If I’m not going to make money doing it, why take the risk?” he asks. In his view, the path to affordability begins with solving the profitability equation for the builder, developer and factory.

That line of thinking is at the heart of Blockhouse’s strategy. Through its CORE housing platform, paired with its CoBuild delivery model, the company is striving to reduce friction between factory efficiency and buyer customization. It provides modular builders, developers and site contractors with a way to preserve repeatability and margin while still offering buyers a meaningful degree of customization.

Housing as a Product Platform

According to Holmes, CORE begins with a simple yet consequential shift in mindset: treating housing more like a product platform than a custom project. “The house is built the same way every single time,” he says. “It’s how you purchase and configure the parts and pieces that make it unique.” That repeatability, he argues, allows the factory to forecast production, control purchasing and maintain efficient output in a way that typical custom modular work does not.

Customers, meanwhile, still want homes that reflect their lives, family size and budgets. How to satisfy these seemingly contradictory needs?

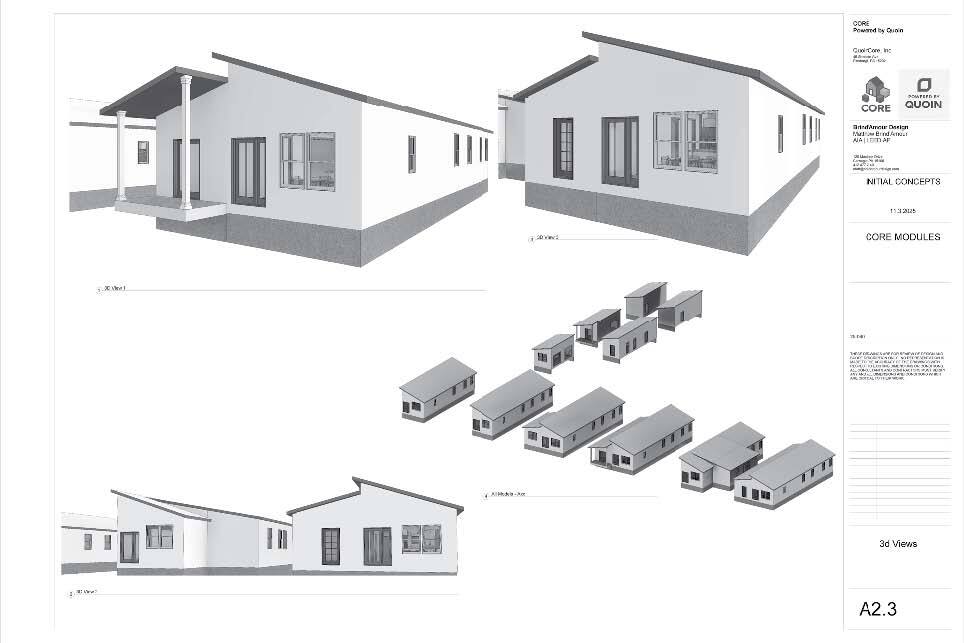

Holmes’ answer is a standardized, low-cost base unit – a one-bedroom CORE – paired with a catalog of attachable accessory units: bedrooms, living rooms, dens, bathrooms and other spaces. Although the base product remains constant, the configuration around it can change.

He compares the concept to the auto industry. A Toyota Corolla is not engineered from scratch each time a buyer wants a different trim package; it starts from a repeatable platform. “With CORE, it’s the same thing over and over,” he says. “The long-term benefit is that, because you have this product, you can begin to truly implement back-end service models for the homeowner that don’t currently exist.”

A Longer-Tail Business Model

Such a distinction matters to builders because it shifts where profit can arise. In the conventional homebuilding model, profit is concentrated in the initial transaction. Once the home is occupied and the final payment is made, the relationship largely ends. Holmes sees CORE as a way to build a longer-tail business around upgrades, accessory additions and ongoing service. As he describe it, the system opens the door to a “membership” model in which homeowners can return for a new bath module, a living-room addition, or another pre-engineered upgrade rather than entering a disruptive, traditional renovation process.

For modular builders, this is more than a design idea; it is also a margin-management strategy. If some long-term profitability can be shifted to accessory sales, service, refurbishment and repeat customer engagement, the initial home can be priced more aggressively without eroding overall profitability.

CORE is designed to simplify future home expansion. Each home has what Holmes calls “portals” — framed door openings in appropriate spots for future accessory units — built into the walls. The portals are then filled in with framing panels and covered with drywall. If someone wants to add a living room at some point, the only interior demo that needs to be done is removing the drywall for the needed opening size. The exterior siding still needs to be removed, but HVAC, plumbing and electrical runs in the CORE are configured for easy connection to the accessory units.

“You just pop the portal out, put the living room on, and you’re done,” he says. The advantage is not only faster installation later, but also greater predictability for factories, site crews and service personnel.

That predictability is central to Holmes’ broader claim that housing can be financially stabilized when treated as a product. “Housing as a product simplifies everything for everybody,” he says. “It gives them stable information to start working from, as opposed to starting fresh.” For developers, that means clearer pro forma statements. For realtors and community groups, it means a more understandable offering. For lenders and insurers, it means a clearer risk profile.

Factory Efficiency on the Jobsite

The CoBuild model extends that logic to the site. Holmes describes it as a more structured, less risky version of the old modular dealer approach.

The home is still largely completed in the factory, but Blockhouse aims to support the buyer and local contractor with a clearer process, guidance and standardized information. “We want to build a system that educates and empowers our customers,” he says, so they can get “a high-quality, well-built, modular home delivered and set where it’s 90% complete” while removing much of the burden from the site contractor.

That point should resonate with smaller builders and site contractors deciding whether to enter modular construction. Holmes argues that the local contractor can reduce liability, cut much of the uncertainty associated with site-built construction and take on more projects per year because so much of the work is already completed in the factory. “The site contractor could build five times as many houses in a year and make the same profit margin,” he says, because the modular approach reduces scope while preserving value.

From a business standpoint, CoBuild reduces coordination friction without forcing local contractors to become full-fledged modular experts overnight. It also aligns with one of Holmes’ central arguments, namely that profitability is not just about factory throughput. It is also about eliminating overruns, delays, excess site scope and coordination failures that erode margins in the field.

Matching Financing to Offsite Construction Realities

Of course, even a disciplined product and delivery strategy like that being offered by Blockhouse can stall if the financing side does not support it. That is where Tom Coronato, Senior Vice President of Construction Lending at CalCon Mutual Mortgage (based in San Diego, Calif.), reinforces this article’s central theme from the lender’s perspective.

Coronato has spent nearly three decades in modular lending and says that many financing barriers stem less from actual risk than from lender misunderstandings. “It’s not that modular is risky,” he explains. “It’s that the banks don’t know how to evaluate the risk correctly.” Traditional lenders are accustomed to advancing funds against work already in place on-site. Modular does not fit that pattern because the factory often requires upfront deposits and full payment before the home leaves the plant.

That timing mismatch creates a cash flow problem that can quickly undermine profitability. Coronato mentions that “the modular manufacturer is grabbing procurement money for materials, but the bank wants to lend only on what’s already on the property.” A builder or developer may have a sound project, but if the lender cannot accommodate the realities of offsite production, the deal becomes harder, slower and more expensive to execute.

Coronato argues that the right lending partner can remove much of that friction. “Partnerships are everything in this business,” he says. One of the biggest obstacles, in his view, is the use of lender “overlays” — internal credit and policy restrictions that go beyond program requirements and trigger avoidable denials. “You’ve just created friction in your process,” he says, referring to sending borrowers to lenders who do not understand modular. That friction creates doubt, delays, extra credit pulls and often a dead deal.

Making Lenders More Comfortable

His comments also support Holmes’ emphasis on standardization. Coronato notes that the industry often overwhelms consumers with too many floor plans and choices, which inevitably slows production and blurs the value proposition. “They shouldn’t have that many choices,” he says, then refers to the auto industry, stating, “You don’t get 4,000 cars to look at. You get three.” He adds that repetition is what makes production work. “When your guys are on the line, they’re trained to do things. What’s better than training? To do the same thing every day.”

Such an observation could be construed as a financing-side endorsement of the CORE philosophy. A narrower, more repeatable product line can improve builder margins, increase factory output and make the project easier for a lender to understand. Coronato also notes that construction-to-perm lending (where a lender’s construction loan is converted into a permanent mortgage for the home-buyer) can help builders get paid more quickly and realize profit sooner. “They can actually shrink the time to be paid to where they’re realizing profit margins much sooner, which means they can lower the price [without affecting margins],” he says.

How Buyers Experience Affordability

Coronato adds another important insight — affordability is often experienced by the buyer as a monthly payment, not the sticker price. “When the bank is willing to partner with the builder and the builder is willing to partner with the bank, they buy down the interest rate for the buyer. Yes, the cost goes back into the home price, but no buyer has ever complained that they financed their rate buy-down. All they look at is the reduced monthly payment.”

Holmes makes a parallel point when discussing markets with low real estate comps. In neighborhoods where existing home values are too low to support the cost of conventional new construction, CORE’s lower entry cost may allow builders and developers to build a functional home on the lot at a more financeable cost, then add value over time through accessories. “The CORE unit itself is an affordable entry point,” Holmes notes, one that is “very approachable when it comes to comps.”

Adding a New Twist To Existing Markets

CORE also offers the opportunity to address the needs of markets ripe for improvement. Consider disaster relief as one example. Using an enhanced structural chassis in the CORE module’s floor makes loading, shipping and offloading modules easier and allows them to be quickly installed on temporary structures in disaster-stricken areas. Then, as damaged properties get cleaned up and rehabilitated with new foundations, the CORE modulest can be relocated to their permanent locations and owners can pick their accessories.

Why These Systems Matter to Modular Builders

The interplay between product design and finance may be where Blockhouse’s concept is most compelling to modular professionals. CORE is not just an architectural idea, and CoBuild is not just a consumer convenience program. Together, they represent an effort to align four often conflicting priorities: factory efficiency, site execution, buyer affordability and lender confidence.

Blockhouse is still early in proving the model, but Holmes says the company is finalizing a six-unit project in Pittsburgh, Pa. to demonstrate multiple CORE configurations and is also working through the final stages of securing a 100- unit order structured for rapid deployment. “Right now, it’s just about getting the word out,” he says.

Better Systems, Not Lower Margins

How CORE scales remains to be seen. But Holmes is highlighting a problem that many modular builders already understand firsthand. If every house is treated as a custom exception, modular will struggle to deliver on its promise. If, instead, housing can be built from stable, repeatable platforms with disciplined options, both the production economics and the financing conversation begin to change.

This may be the key takeaway for builders and modular business owners. The path to housing affordability should not rely on lower margins but on better ones, achieved through superior systems. As Holmes sees it, solve the profitability issue first and affordability has a fighting chance.

Jim Mahannah is a freelance B2B technology writer specializing in construction, energy, water/ wastewater treatment, and cleantech. He is an engineer, and his work experience includes construction project estimating and management in addition to founding and operating a structural components fabrication company supplying residential and commercial building projects.